What follows is the "Looking Ahead" section of my monthly report to investors to be released in the coming days. There are enough misconceptions, misinformation and downright naive analysis floating around about an impending top or potential bubble forming that I felt this deserved to be separated out on its own.

Being that gauging short, intermediate and especially long-term tops has become an obsession among the most recent generation of market participants, it is worthwhile to occasionally divert attention away from the micro and look at this secular bull market from a reasonable, measured perspective. This perspective relies heavily on lessons learned from secular bull markets of the past, with a special focus placed on the secular bull of the 90s.

Why the 90s? It was the last innovation led rally that was guided greatly by technology, with an emphasis on new and emerging companies revolutionizing the way we communicate personally and professionally. It was a rally that was misunderstood, doubted and criticized nearly the entire way up. It was a rally that was resilient through numerous seemingly disastrous macro events. It was a rally that was also resilient through consistent and persistent overvaluation.

The bull market of the 90s was born from two distinct negative events that influenced psychology (and monetary policy, for that matter) greatly.

The 1987 crash effectively ended the secular bull market that started in 1982. The psychology of the investor class was further damaged by the recession of the early 90s that was exacerbated by events such as the Gulf War, rising oil prices, high unemployment and substantial deficits.

These condemnatory events separated only by a few years resulted in a dramatic shift in investor psychology from what was the pervasive bullish sentiment of the mid-80s. This foundation of skepticism and fear provided the perfect foundation for what would be a historic rally throughout the 90s, taking the S&P 500 up some 300% during that decade.

What has occurred from 2000-2012, effectively set the stage for what we are experiencing now. There is no possibility of a substantial secular bull market being born from a point of outright optimism. Secular bull markets are born from the defeated psychology of investors who have little hope or desire of creating anything substantial out of the financial markets. Instead they have come to focus on cash preservation and alternative asset classes that are driven by the desperation of the avoidance of further financial pain. Due diligence becomes a choice phrase. Risk aversion becomes a wise choice. There is no deviating from this path until the reality of a bull market becomes so cemented in the investors mind once again that the fear of missing out on any further gains trumps the fear of losses. We are, by the way, nowhere near that point now.

The indications of the type of pervasive bullish sentiment that gave way to tops like we experienced in 2000 can be gained only by looking at what investors are actually doing with their capital. Since the equity markets are simply one giant flow chart that shouldn’t be too difficult if you know where to look.

I choose to look in three distinct areas of the market to determine whether capital has lost all sense of rationality, indicating a destructive top is approaching:

1. IPO Activity

2. Activity in what I have termed Phase 4 stocks

3. Activity in what I have termed Phase 1 stocks

Before I begin with an explanation of each of the aforementioned, one of the more popular articles I have ever written had to do with determining tops by watching activity in Phase 4 stocks. Here is the article published to the website Minyanville from early 2011. It is a good reference point to understand the rest of this commentary.

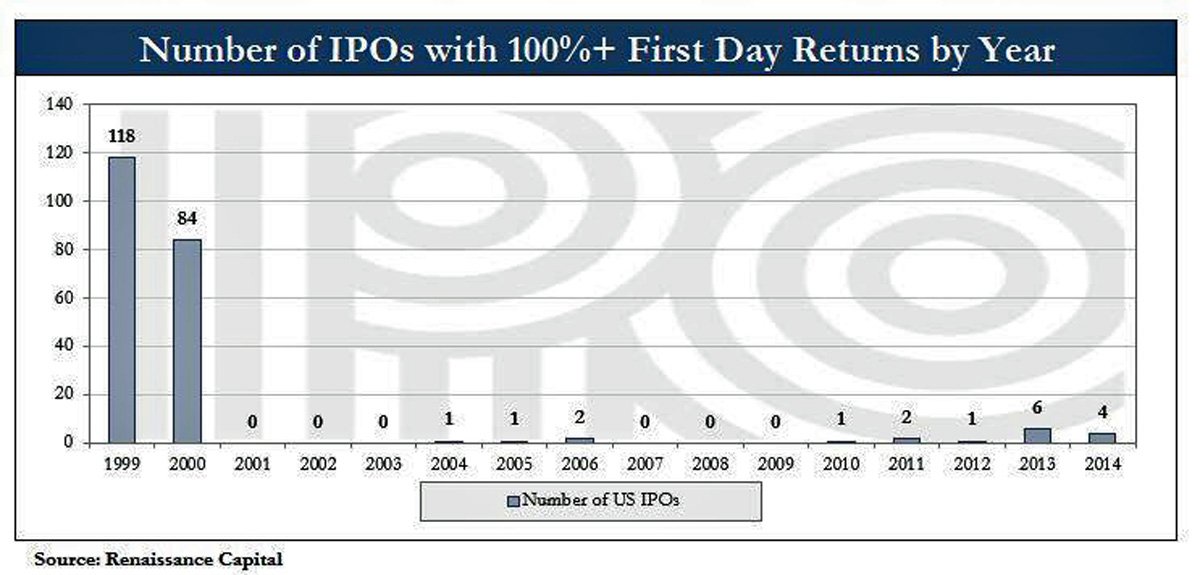

Let’s start with IPO activity. There is a seeming infatuation with loosely throwing around the term “bubble” with one of the primary reasons cited being the failure of IPOs that the market deems irresponsible, less than promising or downright silly. Case in point being the IPO of KING (the maker of the Candy Crush game) just this past week. KING was the worst first day performing IPO in history based on $500 million plus capital raises.

If you were around in the 90s you will remember that the investor appetite for new issues was gluttonous in nature. There wasn’t an IPO that was left to decline for the sake of due diligence. It was simply a game of how high will it go on its first day.

Companies like TheGlobe.com, a social media website, debuted at $9 per share and shot up to $65 by the end of the day. VA Linux had the good fortune of debuting a few months off the market peak in December of 1999 at $30. By the end of the day its shares were trading close to $240. Etoys debuted at $20 per share in May 1999, closing its first day of trading at $76.

As you will immediately notice, there is a distinct difference in nonsensical companies that skyrocket multiple hundred percent during the 90s and ones that end up down 20%, as occurred last week with KING.

What the Wall Street journalists, bloggers, fund managers and analysts seem to be missing entirely is that the ability to bring companies to the public market is a function of good management, a decent idea, a stellar VC team and a hungry underwriter who is eager to collect banking fees. The ability to simply IPO is as much a reflection of investor sentiment as giving birth is a reflection of being an able mother.

The most direct reflection of investor sentiment is the indiscriminate nature of their buying in the most questionable issues. An IPO like KING being offered down on its first day public is actually a reflection of a market that doesn’t yet have that element of indiscriminate buying that indicates a long-term top.

The chart below (courtesy of Business Insider) is as a clear a demonstration as any with respect to lack of speculative capital available for sub-par deals. This is a sign of a healthy market, driven by responsible investors.

Yes, the underwriters have erred, but only in their overestimation of the capital available for these types of deals. The current investor in the markets, generally speaking, remains a diligent one. The next point will expound on this further.

Phase 4 stocks, in case you haven’t read my article from 2011, are companies that are the most speculative. They run at the tail end of a bull market. Their runs are often sloppy, volatile, high volume affairs that have shorts scrambling and longs fantasizing about Monte Carlo and Aston Martins.

These types of names always bring in the tail end of a bull market as investors become absolutely convinced that 20% per annum is no longer enough and they must aim for 150% or face humiliation in the eyes of their peers.

Given that the Phase 4 names rotate every 5-10 years, we must assess what constitutes a Phase 4 stock in this environment? Social media has attracted a great amount of attention, momentum and criticism among investors. We should look not at the top tier names like FB or YELP. Rather we should look down the totem pole at companies like ZNGA, P, and GRPN. The small to mid cap names in the sector that investors who were less prone to investing in quality would gravitate towards purely for momentum purposes.

If you were to look at not just the names I mention here, but any social media name with a market cap below $10 billion, you will not see any high volume, erratic appreciation that indicates a swarm of momentum driven buyers. Instead you will notice steady, consistent appreciation that isn’t excessive in nature as much as it is measured.

Again, this speaks of a lack of momentum driven, “dumb” money in the market to drive these names on ever increasing volume to ever increasing levels of appreciation. Similar to the IPO market, the Phase 4 market remains diligent in nature as opposed to euphoric.

Pandora (P), as an example, is trading only 30% higher than its June 2011 IPO. In almost three years, it has averaged roughly a 10% gain per annum, trailing popular averages by a significant margin.

Groupon is another. GRPN continues to trade far below its IPO price, at levels that would make irrational investors froth at the mouth during a euphoric bull market.

I am not making any argument that these companies are terrific bargains. I don't know anything about them other than what I see in the charts. What I do know, however, is that market participants remain rational enough to pick and choose diligently among the hot sectors. Choosing to stick with the most prominent names in the hottest sectors as opposed to simply pressing the buy button on anything remotely associated. This does not occur during emotional, Phase 4 driven runs that inhibit rationality.

Lastly, it would be beneficial to look at Phase 1 names. What are Phase 1 stocks? They are those names that are the hallmarks of American business. Companies that are in the Dow Jones Industrial Average. Most Americans will have some kind of exposure to these names through pensions, 401ks and mutual funds.

It is important to look at what Phase 1 names are doing because it tells of the inclination of the investor class. In late stages of a speculative rally money will rotate out of conservative bell weathers into speculative names that provide portfolios with a tremendous amount of beta.

Take, for example, the blowoff top for the market that occurred between January of 1999 and March of 2000. During that time the markets witnessed IPOs, as discussed previously, gain 100% plus on a fairly regular basis. Names with little to no earnings power were leading the market higher. Investor cash was indiscriminately being thrown at Phase 4 names at the expense of Phase 1 names.

While multiple hundreds of percent were being returned on investor capital in speculative technology, blue chip names were returning nothing. A clear divergence took place in the final stages of the bull run that caused both retail and institutional investors to rotate out of conservative, widely held names, into the aggressive perceived leaders of the new economy. It got to the point where Warren Buffett was declared an investor who was a has been, simply not understanding the new economy.

Exxon Mobil was flat from January of 1999 to March of 2000.

Proctor & Gamble lost 5% from January of 1999 to March of 2000.

Wal-Mart saw a gain of 19% from January of 1999 to March of 2000.

The Nasdaq Composite saw a gain of over 120% from January of 1999 to March of 2000.

This type of speculative rotation simply doesn't exist in today's market. There is a uniform appreciation occurring that again tells the same story. And that story is one of rational, institutional funds driving this market higher in a very well thought out, deliberate nature. It is not the kind of buying that leads to long-term tops that are created by dramatic asset bubbles.

The institutions that are buying today and in fact, have been buying for the past several years need liquidity to be able to exit their positions in an orderly manner. That liquidity will only come once every investor, institution and those calmly watching from the sidelines embraces the idea that the financial markets can only go up and the opportunity cost of missing out on that upside supersedes any anxiety, trepidation or bad memories they have of past defeats.

Regards,

Ali Meshkati