THE VALUE INVESTOR’S DILEMMA

I don't talk about our positions anymore. Well, scratch that. I do talk about our positions, but only in my monthly letters to investors and during meetings. I've underperformed the markets pretty dramatically over the past 12 months. That's not the reason, however. We are now at a point in this bull market where real opportunities - I'm talking about those that fit my criteria of 300-400% upside in exchange for 20-30% downside risk - are nonexistent. I'm able to find potential doubles out there on occasion, but nothing that warrants replacing any of the names in our current portfolio that have upside of, at least, 200% long-term with minimal downside. Additionally, the rich valuations and excessive risk that needs to be taken to open up a new position in a company that I invariably will understand to a lesser degree than any in our current portfolio makes the framework for new opportunities that much more thin. In other words, something extraordinary needs to pop up to be worthy enough of investment. It didn't used to be this way, of course. In years past, new opportunities would pop up nearly every other month. There were plenty of opportunities in the markets for substantial upside that required very little risk to enjoy. Go through the research section of the website to see all of our past investments. Many of them have doubled, if not more. A few of them have completely fizzled, but we were fortunate enough to sell most at a nice profit in years past. In 2017, I'll be lucky if I write two new reports on small-cap opportunities. I certainly expect to write one, most likely during the second half of the year, once the froth disappears. That one new opportunity may not be necessary, however. Circle of competence and the benefits that are enjoyed by that circle is severely underestimated by a majority of investors. The fact that there are thousands of investments to choose from makes investors think that they need to be Wall Street's equivalent of a Renaissance Man, with a broad swath of knowledge, ranging in investments of all types. That doesn't work, but for a small contingent of professional investors who typically have large staffs. Being an individual investor who attempts this only confuses the process, leading to excessive risk taking, dilution of process and ultimately, plain equity induced confusion. In terms of that circle of competence, there are about 20 companies that I have invested in over the past several years that I have a thorough understand of and am completely comfortable with. Going outside of that circle, again, will require...

DECLINING BOND YIELDS SHOULD HAVE THE ATTENTION OF EVERY INVESTOR

Of the literally thousands of data points available to investors in order to interpret the language of the markets, at present, bond yields may be the most clear. Following the November election of Trump, bond yields jumped higher in anticipation of fiscal stimulus that was the stuff of FDR's dreams. Infrastructure, jobs, manufacturing, growth...it was all coming together in a potpourri of harmonic, capitalistic opportunity that could only result in higher rates. However, somewhere in between election day and the present, the markets realized that while the president is on one page, the rest of the governing body may be on an entirely other. Never mind the fact that politicians are still unsure of the president's message, at this point. Never mind that Republicans are recently suspicious that the center of influence within his administration may be ultra-liberal New York Democrats. Never mind that policy seems to shift on a whim. The entirety of Congress is unsure what they are dealing with, resulting in our current circumstance. The fact that bond yields are now deciding to fall in the face of the most dynamic fiscal stimulus package since the Great Depression is a resounding no-confidence vote against the current administration. Bond yields, after all, are coming up from historically ultra-low levels that should easily be able to support higher rates if the president's message rang true to the ears of the market. One must surmise then that either the market is deaf, dumb or disenchanted by what has been presented up to this point. Bonds yields aren't supposed to falling at this stage of the Trump presidency. The fact that they are is cause for the perking of ears and the sniffing of the surroundings for investors. Stay...

THE PRIMARY LEADER FOR THE CURRENT BULL RUN HAS BROKEN DOWN

While there is continuing reason to believe that the foundation remains in place for further upside to this bull market, cracks are beginning to emerge in the underlying technical foundation. Earlier in the week I highlighted the primary Trumps trades being in the beginning stages of unwinding. Now there are very obvious signs that primary leadership for the market, at the very least, needs a prolonged period of rest. Below is the chart for the SOX (Semiconductor Index), which has been a bastion of absolute strength and leadership for the entirety of the ascent from the February 2016 lows. The trajectory off those lows, for the first time, has been compromised on a weekly basis. click chart to enlarge When you look at the current market, it's becoming obvious that investors are having a difficult time rectifying increased exposure with a near non-stop symphony of scary headlines. Whether increasing geopolitical risk on virtually all fronts or increased domestic fiscal policy risk, the reasons to sell are numerous, while the reasons to buy are scant. That very dynamic, however, could end up being the bulls best hope. Fear remains too high for any substantial pullback, UNLESS a geopolitical event or overwhelming signals of an economic slowdown interfere with the sentiment dynamic. That sentiment dynamic is best illustrated by the long-term moving averages of the combined put/call, which are telling a story of absolute disbelief in a market at record highs. Whether further upside awaits or a breakdown is imminent, the markets are no longer on the solid ground that allowed for studies like this to emerge in Q4 of last year. It's a coin flip going forward. Disclaimer This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice. This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website. T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management...

ARE THE TRUMP TRADES IN THE BEGINNING STAGES OF BEING UNWOUND?

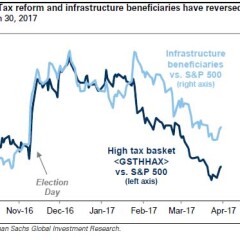

It always seemed fairly obvious that the markets, for better or worse, would test the entire thesis behind all the Trump trades investors put on after he was elected. From yields, to financials, to the US Dollar, every single perception of what should thrive under the capitalist orgy that is the Trump administration would be put the test. Already some of the "no-brainer" stocks that would benefit the most from Trump have unwound. Surprisingly enough, some have completely unwound. Below is a chart of high tax companies that have the most to gain from aggressive tax cuts, plotted side by side with infrastructure beneficiaries. Both of these baskets have unwound their post-election gains completely, with the high tax basket actually showing a loss since election day as of March 30th. Something else is just starting to gain momentum, however. Some rather trustworthy macro indicators of economic health that should be thriving if growth prospects brought on by massive fiscal stimulus were indeed true are beginning to look like they want to reverse course. 10 year treasuries are gaining ground while the Fed is in the process of raising the Fed Funds rate. Bond investors seem to think that economic growth prospects are tepid at best moving forward. click chart to enlarge And then we have Copper, a leading indicator of economic activity that seemed to love Trump during November up to February, but is now deciding that perhaps the need for material for infrastructure projects won't be coming to fruition anytime soon. Finally, financials have been an enormous beneficiary of all the promises of deregulation ushering in what will perhaps be a golden age for the sector in the years ahead. Yet, there has been some lag as of late and suddenly, financials look like they are perfectly content skipping the formalities of any golden age that has been promised. All of this, at the very least, warrants close watch in the weeks ahead as geopolitical fears become amplified, earnings come in fast and furious and the threat of a government shutdown into the end of the month...

ONE FOOT OUT ON TAX REFORM

Donald Trump speaking in an interview with FOX Business that aired today: "You know, if you look at the kind of numbers that we're talking about, that's all going back into the taxes. And we have to do health care first to pick up additional money so that we get great tax reform. So we're going to have a phenomenal tax reform. But I have to do health care first. I want to do it first to really do it right." With these words the president has officially taken one foot out of the water in pursuit of tax cuts. The support for a repeal of Obamacare has faded in light of the intra-party upheaval that caused the first attempt to fall through. Now Republicans have to deal with the fact that their voter base, made of the working class who benefit most from Obamacare, will be left deserted by new legislation, leaving many millions uninsured, alienating a voter base that is quickly pulling back support of a president with some of the lowest approval ratings in the first few months of taking office in history. Trump has to know this. So coming out, basically saying that tax reform is dependent on Obamacare being replaced is setting the stage for an exit on tax reform during the second half of the year. That exit will either consist of a much lower tax cut than most expect, somewhere in the vicinity of 28% for the corporate rate. It is also entirely possible, if not probable, that nothing happens at all, especially if his popularity continues to wane and tax reform gets pushed back to 2018, when mid-term elections take place. And then there is the possibility that the president may have recently realized that geopolitics is much easier than dealing with Congress, making it difficult to focus on the domestic front when there are so many challenges internationally that can be pursued without Congressional approval. Bottom line: Tax reform is hard. Neither Congress or the White House is equipped to deal with hard at the present moment or in fact, for the foreseeable future. Throw in easily distracted leadership and one can see how this goes further and further off track....

QUIET LUSTING FOR A BULL MARKET TOP

There is a certain quiet lusting taking place among investors for a bull market top. The difficulty in creating a logical foundation for a bull market that, according to popular misconception, should have never been in the first place. A bull market that is perceived as being propped up on an artificial platform, buoyed by monetary stimulus, backed by unreasonable valuations, flying in the face of geopolitical fears. The very same reasons the markets should not have climbed in 2011, 2012, 2013 and so on are being cited today. Now this is not to say the market will not correct. Every healthy bull market takes on some measure of correction. In fact, given the nature of this bull market, the next major correction to come will likely fool most everyone into thinking it's the beginning of a substantial bear market. There is, after all, much more "data" to hang your hat on if you're bearish, which serves the counter-intuitive purpose of prolonging the secular bull market. Very simply, it's still too easy to be bearish. It's too easy to look at the numerous valuation measures and determine we have come to far. It's too easy to read the headlines and determine the geopolitical stage is much too unstable. It's too easy to look the monetary policy and determine that the markets won't be able to cope with not having the Fed on their side. It's too easy to look at earnings and determine they aren't growing fast enough to support valuations. Easy, however, doesn't work. Markets are inherently illogical or rather, difficult. Throwing out logical, easy assumptions to gauge the behavior of an illogical, difficult force is an investor's path to mediocrity. Failing to realize that secular bull markets are an expansionary force is a fatal mistake that investors only seem to grasp in the final stages of a secular bull. Let me briefly explain. Expansion during a secular bull market doesn't simply take place in the prices for assets. It takes place in every measure of those prices, as well. An average P/E ratio of 25, for example, could be seen as an extremely rich valuation. However, secular bull markets create new realities for what "extremely rich" constitutes. This goes for everything from sentiment measures, to measures of leverage and of course, valuations. They all expand into areas that are intellectually impossible to conceive or grasp. Abstractions begin to take their form in reality. Therefore, it may be beneficial for investors to begin training their mind in abstract concepts now in order to be able to deal with what is to come. An exercise that is certainly more...

MARCH CLIENT LETTER: CONFUSION IS THE PATH OF LEAST RESISTANCE; LEGISLATIVE MORASS; SOME INTERESTING CHARTS

What follows is a section from the “Thoughts & Analysis” portion of my monthly letter to investors at T11 Capital. Confusion Is The Path of Lease Resistance It remains an extremely simple exercise to look at the circumstances surrounding the current evolution of this bull market and determine that it cannot last. Not much has changed since the inception of this secular bull market in 2013. Doubting the ability of equities to ascend remains the path of least resistance. While it is true that bull markets climb a wall of worry, that wall of worry is often times built on facts that markets do not immediately become concerned with, instead choosing to revel in glorious optimism without concern for what lies dormant in the background. In fact, one of the lessons of experience in finance is that markets very often take longer to react to important developments than one would suspect. The emotions of the day very often take precedent over relevant facts, whether micro or macro related, that have very real consequences for the economy, earnings etc. The markets do a wonderful job of behaving in a nonchalant fashion as important changes occur that immediately concern market observers who then decide that given the markets predominance in one direction, their concern is unwarranted. The important fundamental shifts occurring in the background never go away, of course. They simply lie dormant awaiting the moment when the emotional tank of investors moves to empty. This applies to individual stocks just as much as the broader markets. Individual stocks, especially in my favored category of sub-$500 million in market cap, can take months or years to awaken to fundamental developments that have been percolating in the background while the stock price languishes causing a majority of investors to think that their analysis was wrong, when in fact, their analysis was simply on delay. Companies can often times experience multiple years worth of gains in just a few months as they catch up to the fundamental realities that investors suddenly awaken to. Much like a badly dubbed Chinese Kung-Fu movie where the words are heard before the mouths of the actors begin moving, there is an inherent delay in individual equities and the markets in realizing important fundamental developments. More often than not, the confusion that most investors experience is a result of this delay, giving rise to often used descriptive terms to describe the markets such as illogical, counter-intuitive and contrarian in nature. Markets may, in fact, be much more logical than we realize. However, they are also much less efficient in factoring in relevant developments than we realize, as...