What follows is a section from the “Thoughts & Analysis” portion of my monthly letter to investors at T11 Capital.

Taxes

Like most in the business community, I have been keeping up closely with the tax debate. It carries a special place in my heart as I carry the double edged sword on my back of having to potential to benefit from passage of Trump's tax plan while having a primary investment that will benefit more from its failure.

The one page tax manifesto that took 100 days to develop was underwhelming to say the least. There are a multitude of issues that won't allow for passage in its current form, whether the fact that favoring pass through entities for the lowest corporate tax rate of 15% while leaving the top individual tax rate above 30% creates millions of wealthy individuals who simply funnel their income through corporations. Or the fact that even with the most generous dynamic scoring, the tax plan is a plague to the deficit within an already deficit laden government.

JP Morgan economists Jesse Edgerton and Daniel Silver had this to say about the issue of deficits, "The Congressional Budget Office has scored every 1 [percentage point] reduction in the corporate tax rate with a budgetary cost of about $100 billion over 10 years," Silver and Edgerton wrote. "Thus, reducing the corporate tax rate from 35% to 15% would be scored as adding about $2 trillion in deficits over the next 10 years."

In order to incorporate a deficit of this nature into the budget over the next 10 years it will require bipartisan support. Dangling the carrot of childcare benefits within the tax plan, as one example, in order to entice Democrats was a valiant effort. However, short of making the state of Florida a habitat for endangered seals while giving families making less than $50,000 a year a new Cadillac, President Trump will have a difficult time having a single Democrat supporting a tax plan that favors corporations that are already making record profits and wealthy individuals that have benefited inordinately since the end of the financial crisis.

The only other way for the tax bill in its current form to pass is through the reconciliation process, which would avoid a filibuster by Democrats in the Senate. The dilemma here is that the reconciliation process doesn't allow for a projected increase to the deficit 10 years after the implementation of the plan.

In other words, the Trump plan, in its current form, is virtually impossible to pass. The plan will need to become more deficit friendly in order to be implemented. Meaning, in the end, the corporate tax rate will fall somewhere between 25-30 percent, if the tax plan passes at all.

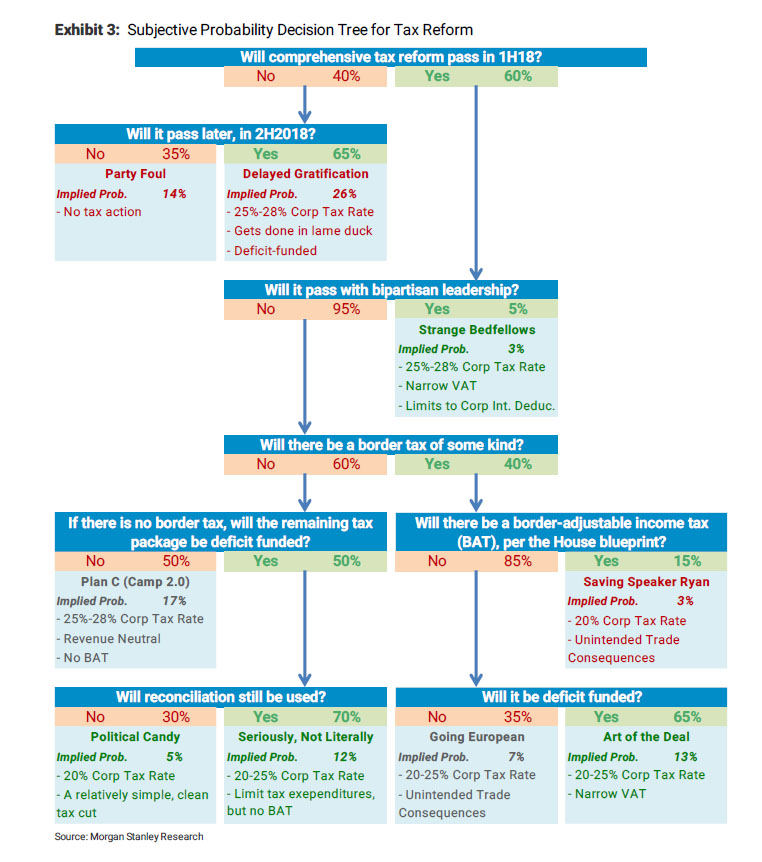

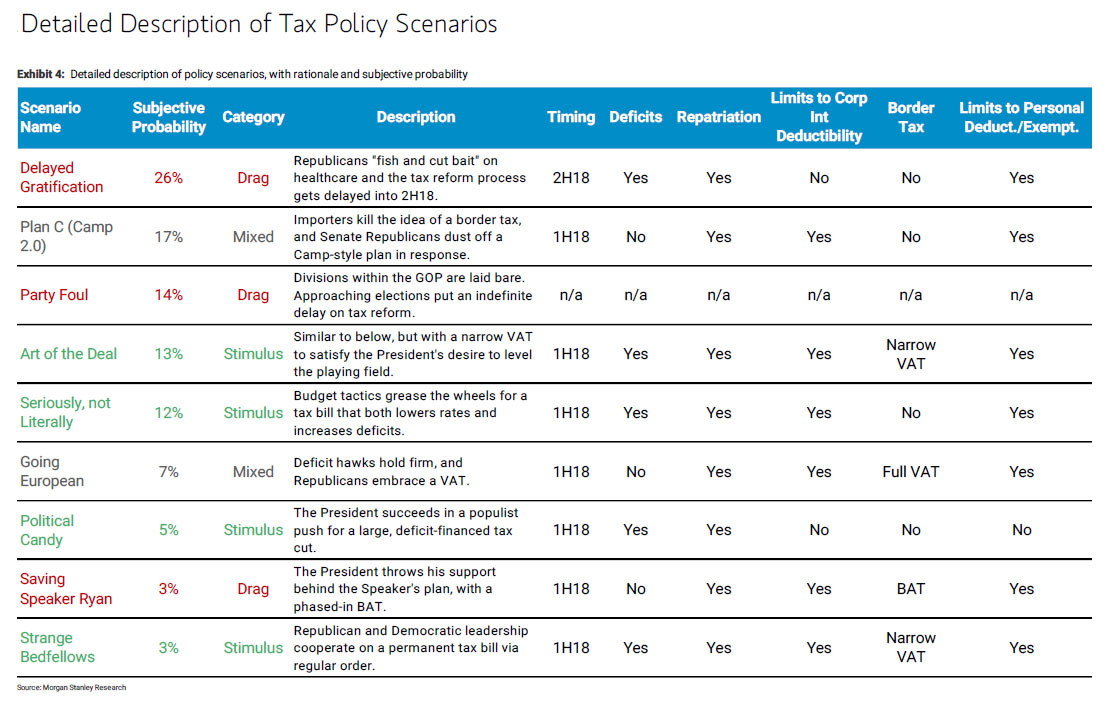

Shortly after Trump's tax plan was introduced, Morgan Stanley came out with a probability matrix that assigns the probability for passage in a variety of forms. The bill is not slated to pass in 2017 in any form. They put a 60% probability of it passing during the first half of 2018. If it doesn't pass by the first half of 2018, there is a 35% there will be no tax plan at all.

The most likely outcome according to Morgan Stanley is a tax plan that passes in 2018 with a 25-28 percent corporate tax rate.

;

There are so many intangibles with the current administration that make the difficulties of passing tax reform that much more arduous. It has never been a simple task to pass reform as there are always powerful special interests that are on the losing end of any proposal. Therefore, cooperation and understanding is needed at some level. There is very little cooperation and understanding, even within the Republican party itself. Add in a president for whom a substantial undercurrent of resentment exists from many in Washington and you get the formula for sabotage on many levels.

Leading to the belief that the entire subject of tax reform is headed for a disappointing conclusion in the end.

Boredom, Terror and Satisfaction

While I take a great amount of pleasure in achieving long-term results that are independent from the general market, our performance since inception of the Trump rally has been a bitter pill to swallow. Watching the market take on an energy and vigor that I have known full well it was capable of achieving, while basically watching from the sidelines, has been a difficult exercise in patience, marked by moments of frustration.

This is the nature of our strategy, however. We are not growth investors who seek out high beta, alpha charged performance at any cost, constantly shifting our exposure as the market dictates. Nor are we aggressive traders who must participate in varying markets, with a preference for volatility and leverage. I am patient with our investments when they require patience, while at the same time having a high probability of rewarding us greatly for our time and commitment.

At the core of what I do is a belief, based on countless observations, that small companies with non-traditional structures, difficult to value assets and outstanding management teams/partners, will outperform most other publicly traded securities over the long-term. There are times when that value becomes apparent almost immediately, as was the case with Impac Mortgage two years ago. And then there is the more typical route, where value takes time to unlock over a very lumpy road, marked by long periods of boredom, interrupted by moments of both sheer terror and immense satisfaction.

To look back at our past investments is a lesson in this dynamic. BFC Financial (now trading under symbol BBXT), as an example, was a company that was purchased in 2013 in the 2 range, sold sometime later in the 4 range, as the company became mired in really what amounted to scandal given the CEOs near constant battle with the SEC causing the company difficulties in moving forward with their plan of action. It seemed like a satisfactory decision to walk away with a gain of nearly 100% in the name, as it moved back down into the 2 range, where it was drifting listlessly for sometime. In a matter of no time, however, the stock has moved close to $7 a share as its issues have been resolved and the company has been allowed to move forward. The event driven nature of the investment required patience that was eventually rewarded through a substantial gain in a very short period of time.

Knight Capital Group is another example of an investment that we made for a short period of time and abandoned relatively quickly because the upside didn't match what was available in some of our current positions, for example. The stock meandered in 10-12 range for three years before realization of the value inherent in the name created demand that drove the stock to 14 and then it was bought out for $20 per share just recently. Again, this was a special situation that required patience for the market to put two and two together.

The longer we remain exposed to an investment the more likely we will experience the entire range of emotions: Boredom, terror and satisfaction. However, the longer we remain invested the more likely we are to see the investment fully mature. The entire range of emotions is simply the price we pay for the privilege of allowing time to converge with opportunity.

There was an article on Business Insider recently about how rich an individual would be had he or she invested in AMZN at its IPO. These types of articles become extremely commonplace during the type of growth led run we are having in the markets. Many investors will look over the article, thinking to themselves: If I was only so smart as to put my money into the stock at that time, riding my way to riches.

It has nothing to do with smart, however. The smartest of individuals would not be able to deal with the constant cycle of boredom, terror and satisfaction. They would become distracted during the boring periods. Fearful during the terror filled periods and greedy during the periods of satisfaction. Eventually finding a way to get in their own way, despite an initial correct inclination to do nothing. Emotions are not easily forgotten, whereas simple strategic thoughts fall into the background.

The emotion of fear perhaps is the greatest of all. Once fear is experienced in a very real way through the loss of capital, it becomes important to an individual never to experience that fear again through whatever means necessary. That means if you are in a stock like AMZN, suffering a 50%+ drawdown, your next step is to prevent that type of drawdown from happening again. How many periods of sheer terror have taken place in AMZN's journey from its 1997 IPO?

In 1999 the stock lost 63%, causing investors head pain, occasional sleepness nights and anxiety.

Between 2000-2001 the stock lost 95% of its value, causing nausea, anxiety induced psychosis, divorce and base jumping without a parachute.

By the middle of 2003, AMZN had recovered to the tune of 827% on the upside from its 2001 lows. You know what happened next?

A three year slow and deliberate extermination of value as the stock fell by 60% over three years while the general market did fantastic. Investors hated Jeff Bezos.

After recovering from that episode from 2007 – 2008, the stock fell 66%, yet again.

Most companies don't deserve to be held through the entire range of the emotional spectrum. It's too difficult. The reward typically doesn't justify the effort. In other words, those companies that deserve to be held long enough to move through the entire cycle of emotions in exchange for the privilege of time/opportunity convergence are few and far between.

We are in possession of two of them at present, which is a fortunate situation. Both are presently in their own respective boredom phase. The boredom has another element attached to it, however, when every other equity name around us is dancing to a seemingly nonstop symphony of greatest hits while we play the violin alone by candlelight in the basement of the venue.

We have a history of creating value independent of the market. I expect that to be the case moving forward as the party up above us steadily dissipates into the second half of 2017.

And Finally....

Warren Buffet has hired two successors to himself and Charlie Munger who are named, of course, Todd and Ted. Only Mr. Buffett could find a way to ensure that down home, country values extend all the way into the names of his successors sounding like a pair of brothers who own the local garage in downtown Omaha.

Warren, Todd and Ted were all interviewed recently in an interview that made me feel like life could indeed be a sophisticated, nuanced version of The Truman Show.

In any case, I found the description of their days to be beneficial in that it is contradictory to the popular image of your typical “Wall Street guy.” The cliché image of a guy with a headset on, surrounded by 6 screens, screaming orders, talking to various contacts, while turning bright red on occasion is one that doesn't apply to Buffet or his successors.

Here is how they spend their days:

“It’s terrific. In many ways, it doesn’t change much from my prior world, where I ran a fund,” Weschler says. “I’ve always been kind of a one man band, analytically. I spend the vast majority of my day reading. I try to make about half of that reading random. Things like newspapers and trade periodicals,” Ted says.

And Todd's day isn't much different: “I get in around 7 or 8, and I read until about 7 or 8 at night,” he says with a laugh. “And I go home, and see my family, and then I’ll read for another hour or two in bed at night. And you know, there might only be three to four phone calls the entire week. So there are very, very few interruptions. I have a great assistant who knows everything that I read, and she kinda provides everything, and there’s a back and forth between us where I’ll mark it up, and give it back to her. And we have a system for filing and so forth. But it’s literally just reading about 12 hours a day of everything I just mentioned.”

Berkshire Hathaway is a library that makes investments on the side. That's a valuable business model for any investor that doesn't understand the nature of investments is to invest.

Regards,

Ali Meshkati