There are presently three distinct factors that have a high probability of being misunderstood by investors. This misunderstanding has created a slingshot effect in the market, where viewpoints have been pulled back to maximum tension, with the potential release in the opposite direction being unlike anything we have experienced in recent memory, creating one part of The Great Acceleration Cycle. The three misunderstood factors are as follows:

1. Virus

2. Economy

3. QE

Virus: Over the past week, we have started to see a significant amount of evidence that the numbers used to justify what is basically a complete shutdown of the global economy were inflated substantially. It starts with the Imperial College study that was cited by global leaders as a plausible scenario, justifying the shutdown of numerous countries. In that study it was expected that 500,000 would die in the UK. The author of the study last week revised that number down to 20,000 people or fewer.

Given that the Imperial College study was the preeminent research on the matter, this revision was jarring, despite the fact that it was under-reported by the mainstream press.

In the United States, projections had NYC at 61000 hospitalized by April 4th. On April 4th NYC had 14000 hospitalized.

Governor Cuomo today said that the number of deaths has been dropping for the first time. This is happening well before the most optimistic case peak 7 days from now.

Other pieces of data from major cities, include Los Angeles, with one of the largest hospitals in Cedars Sinai having 115 Covid cases on March 31st, up from 50 cases on March 17th. A relatively insignificant increase versus projections.

Internationally, both Italy and France are reporting significant drops in deaths today for the first time.

The alarmist nature of the initial projections, few of which have come to fruition, is the first band pulled to maximum tension on the slingshot.

Economy: The most important factor to realize with respect to current economic projections is that they have been modeled around virus projections. If the virus projections are off, then the economic projections are equally incorrect.

While the job losses and economic ramifications of this shutdown are jarring to witness, projections fail to take into account the effectiveness of fiscal and monetary policy measures, along with the evolution of the job market once the economy reopens.

Other factors include the ability of businesses in food and entertainment to bounce back.

While this view can't be quantified, my sense is that once developed economies reopen there will be a united, patriotic stand that embraces small businesses that have suffered through this. Those who are most susceptible to the virus (60+ and preexisting conditions) will be slower coming back out in numbers. However, the rest of the consumer base will be quick to return, with an almost feverish pitch of spending, boosted by government money and savings created by staying indoors for an extended period of time. This will result in substantial upside to the current economic numbers.

This is the second band pulled to maximum tension.

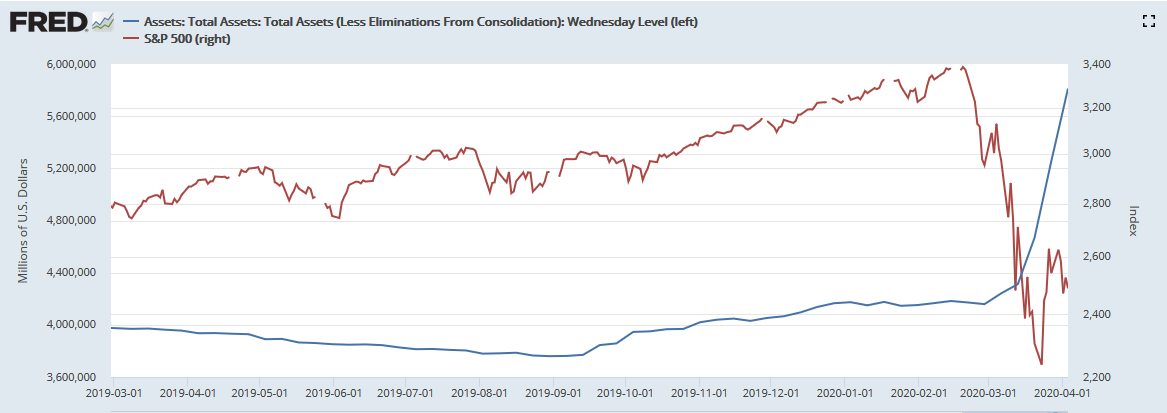

QE: This is the most substantial piece of the underlying puzzle. The most significant development over the past month is that the Fed is now scared. You can tell they are scared by the series of measures they have taken, including emergency rate cuts, purchasing corporate bonds, moving into the municipal market and massive liquidity injections they are throwing into the market on a daily basis.

The steady uptrend in the Fed balance sheet coincided with the market rally beginning in October. The massive acceleration in the Fed balance sheet has been initially met by skepticism as to its effectiveness presently.

A scared Federal Reserve is the most bullish factor in the current market environment because it opens them up to policy errors that have long-term destabilizing effects. Although this sounds bearish, policy errors with respect to monetary policy can result in volatility in both ways. Part of the destabilizing effect created by the Fed being fearful of not doing enough here will be to create massive market volatility the likes of which we have rarely experienced on the downside AND upside.

We've already witnessed that in February and March via unprecedented downside volatility when the Fed is in the midst of QE operations while simultaneously being met with a significant crisis. A confluence of events that has never occurred before.

Over the next several months investors will witness equally proportional upside volatility while the Fed shifts QE policy into hyper-drive. The upside volatility has a significant probability of overshooting on the upside, moving the market to new highs before the election.

This is the third and final band of the slingshot with the most amount of tension.

When released on the upside, all three of these together will result in what will likely be the most significant rally of the past decade taking place over the next six months.

The Great Acceleration Cycle we are experiencing has not just compacted economic policy into a very small window, but it will also compact market volatility that would typically place over a matter of years into just a handful of months.

While this will be greatly destabilizing over the long-term, the short to intermediate term consequences should be taken advantage of to the maximum extent possible by investors.

Zenolytics now offers Turning Points and ETF Pro premium service Click here for details.

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.