What follows is a section from the “Thoughts & Analysis” portion of my monthly letter to investors at T11 Capital.

Sunshine and Rain

The obstacles to the continuance of this bull market are not so much data driven as they are emotionally driven. Every bull market brings with it an abundance of worrying factors that drive investors to the sidelines, thinking that an avalanche of adverse circumstances will take away whatever profits an investor has accumulated during the bull run.

Since the beginning of this secular bull market investors have been bothered by a confluence of data that lend credibility to the thought that a collapse was imminent. It is only recently that investors have evolved from that line of thinking into a more solid foundation for investment. That foundation has allowed the market to move forward, nearly unencumbered since the election. At the very same time, the confidence created by such a foundation has, for the first time, opened the doors to extreme volatility that isn't currently being reflected in the popular volatility gauges.

The fundamental foundation for investment that currently exists is based on fiscal stimulus measures that are varied in method. They encompass everything from incentives toward domestic manufacturing to infrastructure spending, with foreign allies recently stepping up to the plate to assist in the financing of such projects. Of course, tax cuts are being rightly seen as the master key towards unlocking a treasure chest of corporate profits.

The current White House has very obviously been the trigger for the tectonic plates beneath the markets shifting substantially since the election. Therefore, it would make sense that when the current administration is threatened, the markets would feel threatened, as well. It would also make sense to consider that when the current administration is encumbered by investigations into their conduct, regardless of the merits of the investigation itself, that markets would accurately surmise that a delay in the fiscal stimulus agenda is a very real possibility.

In fact, Goldman Sachs came out recently with a completely modified forecast for what lies ahead for tax legislation, saying the following:

The probability that tax legislation will be enacted by 2018 has fallen further, in our view, as a result of recent events. The last few weeks have taken a toll on President Trump’s approval rating as well as support for Republicans in Congress.... Over the last week, the President’s approval rating has averaged around 40%, and Democrats have led generic ballot polls over the last week by an average of 11 points.

It is also not clear how much support there will be for a simple tax cut. The White House has proposed a tax cut that we expect might cost $3-4 trillion over ten years but House Republican leaders have insisted on revenue-neutral tax reform that does not add to the deficit and earlier this week, Senate Majority Leader Mitch McConnell called for revenue-neutral tax reform as well. While their definition of “revenue-neutral” includes dynamic scoring and other technicalities that might be worth several hundred billion dollars over ten years, even under a loose definition of “revenue neutral” this would seem to preclude a substantial net tax cut.

In light of these developments, we are changing our fiscal policy assumptions. We already assigned a very low probability to comprehensive tax reform by 2018 but recent events make it even less likely in our view. Our base case has been that Congress would enact a reasonably simple corporate and individual tax cut, with incremental reform—limited base broadening and international corporate reform—that would reduce revenues by $1.75 trillion over ten years.

However, with little evidence so far that Congress is moving in the direction of a substantial net tax cut and the continued focus on revenue-neutrality we have seen from congressional leaders, we have reduced our assumption to $1 trillion over ten years, which reflects an expectation of a tax cut that could be considered close to revenue-neutral under the loose definition that congressional Republicans have been using. This could allow for a modest personal tax cut and, with a few budgetary offsets, a reduction in the corporate rate to 28%. We continue to believe that some type of tax legislation is more likely than not to be enacted in early 2018, but this is also now a much closer call than it used to be, in our view.

And how does the market view the potential for tax reform going forward? Here is an updated look at the performance of a high tax rate basket of companies, now trading well below where they were even before the elections.

Political risk, in all its colorful forms, has suddenly become a very real consideration for much of Wall Street. So much so, in fact, that the infamous Jon Corzine recently announced a hedge fund that seeks out opportunities to profit from the coming political calamities that may befall the financial markets. While a hedge fund that focuses on political calamities doesn't necessarily sound like a diligent use of resources, the point is well taken. We are living in a climate of extreme political risk the likes of which, we have arguably, never experienced.

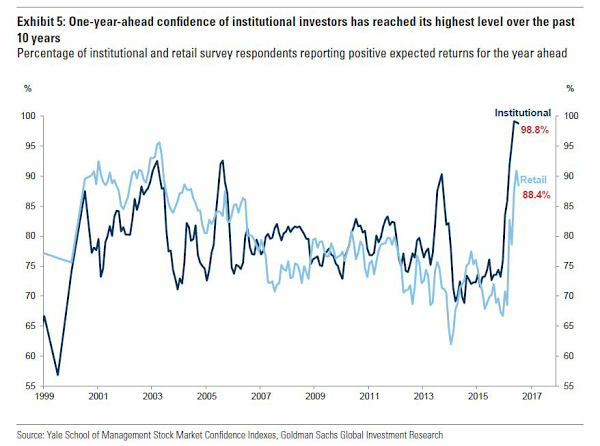

All the meanwhile, investors have become enamored by the momentum of the markets, in what is really the first such complete and total loyalty to stocks of this secular bull market. As can be observed in the chart below, investors, both institutional and retail, have complete faith in returns for stocks going forward.

This type of unencumbered optimism in stocks has led to volatility being pressed to the point of, seemingly, no return. As a result, either shorting the popular volatility based ETFs or going long inverse volatility ETFs has now become the hot trade among both hedge funds and retail investors. For example, assets under management of inverse VIX Exchange Traded Products (such as the XIV) has grown $600 million year to date while assets under management in long VIX products have declined $460 million.

More astoundingly, short interest in volatility related products has now gone parabolic, as investors become anchored to the current environment of steady gains with little volatility.

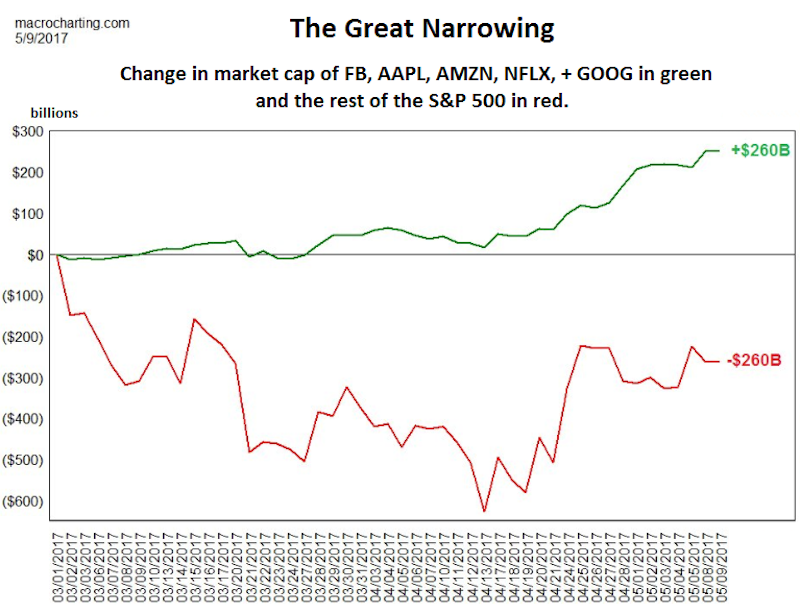

Needless to say, we are in a market of some pretty distinct outliers. Perhaps none more so, however, than the fact that the FAANGs (Facebook, Amazon, Apple, Netflix, Google) have gained $260 billion in value, while the other 495 companies in the S&P 500 have lost an identical amount.

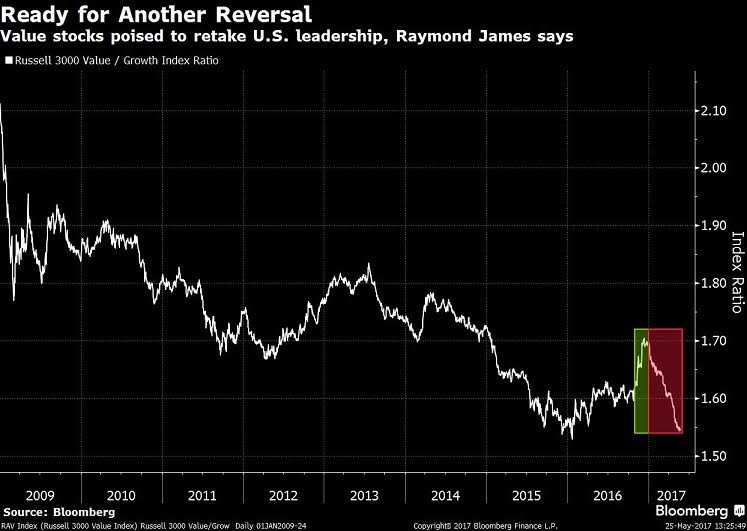

Of course, we have not walked away from this lack of balance in the markets unscathed. The preference for growth over value is more pronounced now than at any point in this bull market. Making the markets extremely difficult for value oriented managers.

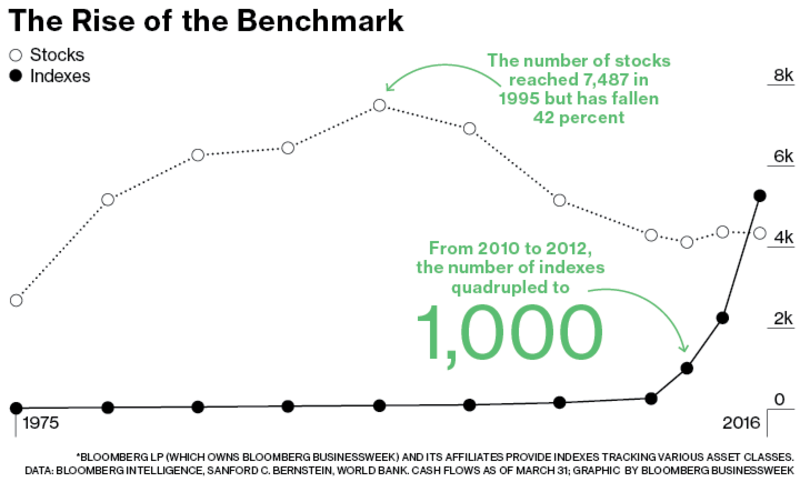

Making things further difficult is the fact that the stock market is no longer a market of stocks. Rather, the stock market has become the ETF market. Individual stocks no longer attract the attention of investors, who seemingly have developed a fondness for quant strategies surrounding ETFs. The ETF manufacturers are only more than happy to supply this demand through every type of ETF imaginable, pulling considerable volume away from equities into ETFs. Astoundingly enough, for the first time in U.S. market history, there are more indices/ETFs than there are stocks.

As one can easily observe, there are an astounding array of imbalances taking place in the markets presently. Those imbalances have created an environment that should dictate to investors a sense of alertness and caution that has not necessarily been a required trait at any point in the past seven years. With increasing imbalances comes the necessity for the market to take extreme measures to correct them. This reality dictates caution as we move into the second half of 2017.

Are Millenials The New Phase 4 Investor?

Way back in 2011, I penned a piece named, “All Phase 4 Investors Gather Around, I Have News For You.” The blog posting described a very consistent phenomenon in the markets of a certain group of individuals showing up in the markets during beginning, mid and late stages of a cycle. Those investors who arrive at the late stages I deem to be phase 4 investors who tend to focus on ultra-aggressive assets, signaling the bullish thesis moving full circle with their arrival.

Of course, it is a well known fact that millennials are a risk averse generation, witnessing various financial calamities involving both real estate and equities. They have not experienced anything at all resembling a consistent, steady trend in a financial asset that allows them to actually have trust in the financial system.

That is until recently. In 2017, certain indications have taken place that point to a thawing of the hearts of the millennial crowd towards risk. First, they have started to actually not only purchase homes, but flip them, as well. A recent LA Times article profiled “flipsters.” Hipsters who have taken a liking to flipping homes over the past several years. Their target clientele are other millennials who are, for the first time, looking to buy instead of rent.

Second, the unencumbered strength of the hottest names in technology have millennial fingerprints all over them. Amazon, Apple, Facebook, Netflix. These are all companies they know and have been gravitating towards, no questions asked. Lest we forget, the luridly overpriced IPO of SNAP was greeted warmly by millennials. A technology IPO getting the attention of the “financial markets are rigged” generation marks a tangible change in the negative psychology that has persisted since the financial crisis by the younger generation.

Finally, perhaps the strongest indication of complete and total acceptance of risk among millennials is the astounding ascent of the cryptocurrencies, led, of course, by Bitcoin. Bitcoin has increased by some 1,000% over the last couple years. A study led by Facebook recently found that 92% of millennials do not trust banks. The alternative, in their view, is to circumvent the banking system through an entirely new means of creating, storing and transferring capital.

Bitcoin is the modern day proxy for the comfort that exists with technology investments. It is no coincidence that key technology names are ascending at a rapid pace alongside Bitcoin. It is all a reflection of the comfort that exists with technology as a store of wealth in the current economy. That comfort comes at a price, however.

Financial markets typically don't function well when large groups of investors become comfortable enough to chase prices to unreasonable heights. It creates capital imbalances that markets invariably correct through prolonged periods of punishment, rinsing nearly every participant that was comfortable with their investment in the prior cycle.

The fact that Bitcoin has now joined real estate and equities in a speculative, persistent march higher doesn't indicate the future dominance of this new currency as much as it indicates that equity markets, led by technology, may indeed be in a Phase 4 stage that signals minimal rewards to be had in exchange for an abundance of risk.

One more sign that diligence in one's approach to the financial markets is presently the preferred path forward as lack of concern for risk gives way to the increasing probability of downside volatility.

Regards,

Ali Meshkati

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.