What follows is a section from the “Thoughts & Analysis” portion of my monthly letter to investors at T11 Capital.

The Small-Cap Market of 2016

Since 2014, small-cap investors have been treated to a sideways market, with a 27% peak to valley drawdown thrown in for good measure. The pricing environment for small company shares paired up with a near chronic pessimism that has incrementally advanced since the 2009 bottom has led to a trading environment that is tremendously illiquid and severely mispriced in certain areas.

In small-cap investing, there will always be pockets of mispricing as the market simply is not efficient enough to correctly price thousands of companies with scant or nonexistent analyst coverage. This simple phenomenon leads to the opportunities that become available to investors over time to profit from these blatant inefficiencies in the marketplace.

In 2016, however, the simple phenomenon of mispricing has taken on a new slant. Securities pricing is being graded by difficulty. The more difficult the situation, the more likely it is that the company will be mispriced. Companies that release relevant, easy to digest information regarding products or partnerships that are recognizable to investors are properly rewarded through premiums in share price. However, situations that are opaque, difficult or those possessing variability in outcomes are largely ignored.

This leaves special situation/event driven investors reliant upon their analysis to be correct more than ever because the market simply won't assign a premium based on expectations of success, but on success coming to fruition in a tangible, recognizable way.

In some ways, the public equity market for companies with market caps under $500 million has become similar to private equity or venture capital in 2016. Value is taking longer to realize in an environment that is not necessarily liquid but rewards tangible results over time. Gone are the days of blanket adjustments up in the price of shares based on a sector or general market movement. Companies are being left behind in favor of tangible performers with tangible products and partnerships.

This leaves the special situation/event driven investor in a position that demands a mentality in step with the times. Managers have a relatively simple decision to make:

1. Conform to the current market cycle, seeking out opportunities that the market sees as relevant. Essentially becoming a growth investor rather than a value investor.

2. Adjust your mentality to fall more in line with that of a private equity or venture capital investor that is dealing in the public markets.

Very simply put, assuming that you disagree with the first choice, deciding that maintaining an edge in the markets is superior to conformity, the time frame for investment must be stretched and the barrier to entry for new positions must be fortified. In today's market environment, patience and discretion in and of themselves is a tangible edge for investors.

The markets inability to properly value complicated investments in the small-cap space also means that once these opportunities are properly understood, the valuation creation that takes place will be sudden and dramatic in nature.

Additionally, in the spirit of ever changing cycles, as the small-cap market continues to take steps towards defrosting, eventually reaching all-time highs, investors will, once again, start becoming interested in speculating in opportunities that require slightly more exertion of the mental faculty in exchange for greater rewards.

August Edition of “I'd Rather Eat Rocks Than Buy Stocks”

The bearish equity investing camp seems to have a very consistent modus operandi for remaining in cash or net short equities despite the recent run to new highs in the S&P 500. The majority of bearish investors will reference valuation, of course, as it is always a simple exercise to choose any number of valuation measures to best fit one's argument for overvaluation of equities.

The more distinct and perhaps convincing argument to a world filled with economic skeptics and pessimists, however, is that this global central bank experiment into these extreme, uncharted waters of monetary policy will fail. They are unsustainable and reckless in the end, leading to depressed prices of equities, with economic output globally collapsing after central bankers run out of ammunition is the claim consistently put forward by the bearish camp.

While it is always easy to look at something that has never been attempted, stating that it is doomed to failure in the end, it may be more wise to look at what is actually being attempted here by not just one central bank, but central bank's globally, in cooperation with one another.

Now, there is no arguing with the likes of Charlie Munger, who recently said that nobody knows with certainty what the outcome of this experiment by global central banks will be. What is typical, however, in these types of situations where the intellectual output of individuals converges along identical lines is for the markets and economy to move in the exact opposite direction as widely or logically expected. Illogical, unpopular expectations most often thrive in the markets and economy, making a mockery of traditional economists while forcing asset managers who desire to outperform into divergent positions.

To look at what is occurring in an almost ridiculously simple manner is perhaps the best way forward, without any preconditions related to economic moral hazard or the uncharted nature of the territory we are in. Simply put, global central banks are explicitly stating that they are the new players in the global asset markets. The Bank of Japan is going as far as purchasing equities on the open market. The European Central Bank is purchasing corporate bonds. The Fed has purchased treasuries in the past. This policy of having an active hand in the asset markets is not subject to deterioration over time, but rather acceleration. This is an endeavor that once embarked upon must be consistently followed. To what end? None of us know. All we can do as investors who desire outsized returns is attempt to judge what will occur in the interim.

If global central banks have made it abundantly obvious that they are the new players in the global financial markets, with a limitless balance sheet and appetite for assets, then you can only assume that those assets are subject to an almost unprecedented appreciation over time. We have already seen it in the bond market, with a dramatic dislocation taking place causing what is now $14 trillion in negative yielding government debt.

With asset prices all being interrelated, dislocations in key asset prices spread over time. They are not simply contained to one area, such as fixed income, with equities, commodities and the like being immune to similar dislocations.

Thus far, the dislocation that has taken place in the bond market has caused equities to move into a fetal position of sorts, creating one of the least volatile years of trading of the past several decades in 2016. The daily ranges in the S&P 500 have been some of narrowest on record. This comes as the equity markets are being driven primarily by a search for yield in equity names to replace the nonexistent yields available via fixed income, driving traditionally conservative names in sectors such as consumer staples and utilities to new highs.

This is likely the first phase of moving away from fixed income, with a focus on equities that have yield. As fixed income investors realize the absurdity of investing in assets that costs them capital in exchange for safety of capital, they will be looking toward equities in an incrementally aggressive manner, eventually coming to the realization that it is possible that equities can grow capital at or above historical rates, without the threat of a repeat of 2008 on the immediate horizon.

This realization is a powerful one when you consider two factors:

1. The amount of capital tucked away in fixed income securities by everyone from individuals to institutions and governments. You can see in the graphic below that the appetite for government debt is at what can be classified as panic levels.

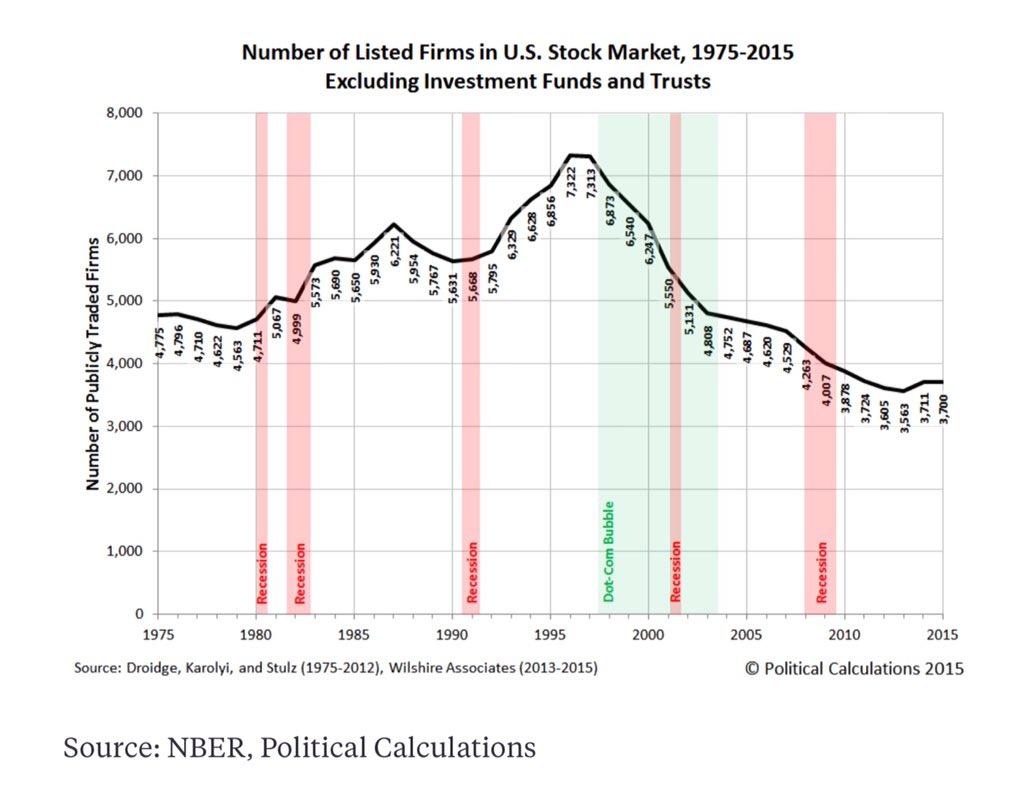

2. The thinning out of the equity markets over the past 20 years via private equity investors, stock buybacks, reluctance by companies to go public and corporate dissolution, bankruptcy etc.

The concoction that has been thrown together for equities at this juncture is an explosive one. All the key ingredients are in place: Abundant pessimism, lack of equity supply, a record misallocation into fixed income securities causing negative yield and finally, central bank support as a buyer of last resort.

The Narrows

2016 is turning out to be a historical year for lack of volatility in the markets. We are seeing a consistent pattern of narrow daily ranges that have historically ranked among the narrowest in multiple decades.

The obvious question is what does such an absence of volatility mean for the equity markets over the long-term?

The answer is decidedly bullish as demonstrated in the chart below.

As can be seen in the chart above, when the 2 year percentage range falls to the bottom of the range at all-time highs it is one of the most consistently bullish long-term signals out there. The last time the market saw anything resembling what we have experienced in 2016 in terms of lack of volatility was the mid-90s, before the markets went parabolic into the second half of the decade, with the S&P 500 tripling in value. Prior to that it was the mid-80s, before the S&P would double over the next few years.

At present, we have the lowest 2 year percent range in market history paired with pessimism that is higher than at any point since the depths of the financial crisis as measured by the long-term put/call ratio.

The fact that investors must overcome the constant psychological hurdle of the mantra of doom and gloom makes the aforementioned facts all the more bullish. In the financial markets, what is psychologically uncomfortable is more often than not the most beneficial decision one can make. It is only when comfort, joy and convenience enter the equation that investors should tuck their tails between their respective legs and run for the hills.

There is no comfort, joy or convenience in equity investment presently, making this an opportune time for those who take pleasure in putting capital to work in ideal conditions.

Regards,

Ali Meshkati

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.