As an investment gold has a cult like following among a rigidly fanatical group of aficionados who like to use words like “fiat” and “ponzi” as often as possible. They discuss the metal as if it has mystical properties that will provide them with protection regardless of the circumstance, having thousands of years of history on their side as evidence of the utility of gold as an investment, a currency and ultimately an insurance policy against all the eventualities of mankind.

For this reason gold is often seen by most investors as an instrument of the paranoid to protect against an unseen, unrealistic set of risks that are so anomalous that even mere consideration of gold as an investment is a waste of time.

Outside of the realm of fanaticism and paranoia, the function of gold within an investor's portfolio is extraordinarily simple: During times of turbulence it acts as an insurance policy. It is effectively an unexpiring put option against monetary policy mistakes; aggressive acts of fiscal stimulus; conflicts between world governments; geopolitical risk AND tumbling equity markets.

Before proceeding any further, let me clear: If it wasn't for the breakout that occurred in 2001/2002 for gold that propelled the metal from the $300 range close to $2000 before experiencing a 44% retracement between 2011 to present day, I wouldn't be discussing the metal at all. In other words, if gold was still sitting at $300 and the massive, long-term shift in the secular trend had not taken place, then it wouldn't be worth mentioning. Gold is only worth discussing because it is now in a long-term uptrend. The move down in recent years is simply a pause in that uptrend, with a resumption set to take place at some point in the not too distant future.

As with everything I do in the markets, the foundation for my interest in gold is technical/pattern recognition driven in nature, further backed by fundamentals that support the technical/pattern recognition data. There are statistically significant patterns being developed in both physical gold and gold miners that are some of the most productive in a market devoid of productive bullish patterns.

Most strikingly, perhaps, is the symmetry that has occurred between the secular low in 2000 for gold and the low in 1970, followed by the behavior in the metal in the years following. Here are some highlights:

- Both lows occurred at the turn of a new decade (1970 & 2000)

- Both lows occurred around shifts in the global currency system (1971 cancellation of Bretton Woods & 1999 introduction of the Euro)

- Both lows occurred after multiple decades of disinterest in gold as an investment

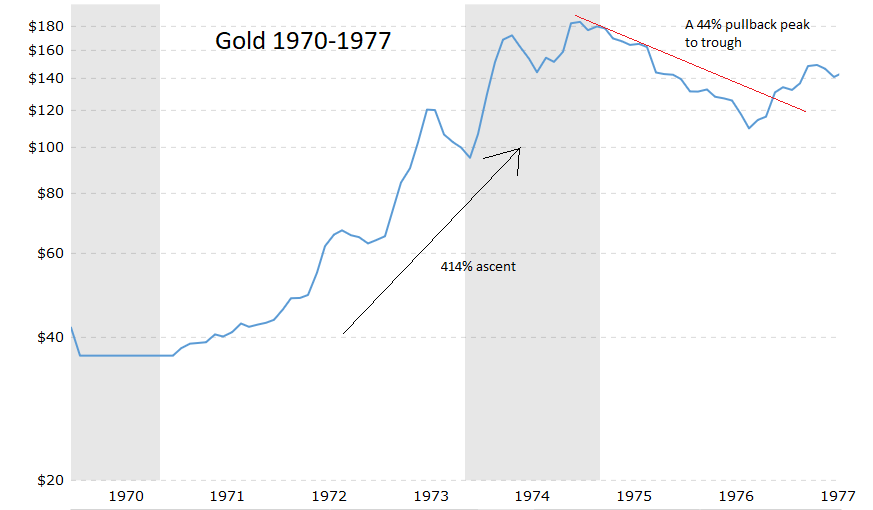

- The rise that took place in the first leg of the move in gold from $35 to $180 during the 70s was 414%

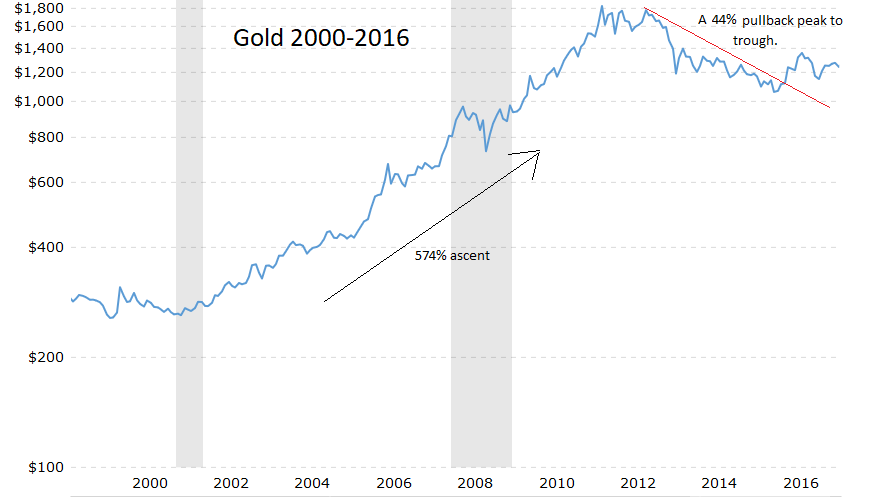

- The rise that has taken place during the first leg of our current move from a low of $280 to the 2011 highs was 574%

- The pullback that took place from the highs of the first leg in 1974 at $197 to the low in 1976 at $110 was 44%

- The pullback that took place from the highs of the first in 2011 at $1888 to the low in ` 2015 at $1056 was 44%

Here is a chart of the 1970s move in gold up to the 1974 high and the 1976 low at $110.

Here is a chart of the move in gold from 2000, to the high in 2011 and the subsequent low in 2015

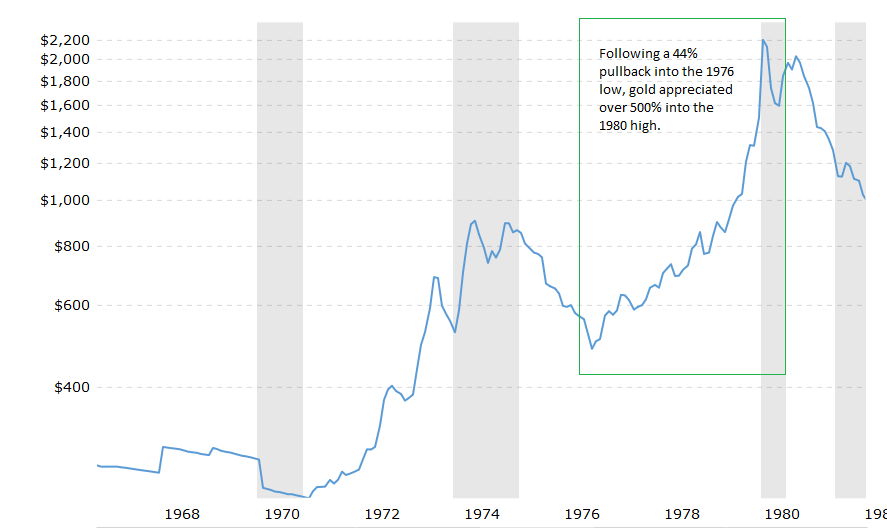

Here is what happened to gold following the 44% pullback from 1974 to 1976.

Apart from the technical prowess of gold, the fundamental data is extremely compelling. Since gold doesn't have a P/E ratio or any other traditional measure of value, ratios to other popular asset classes are one way to measure the value of the metal.

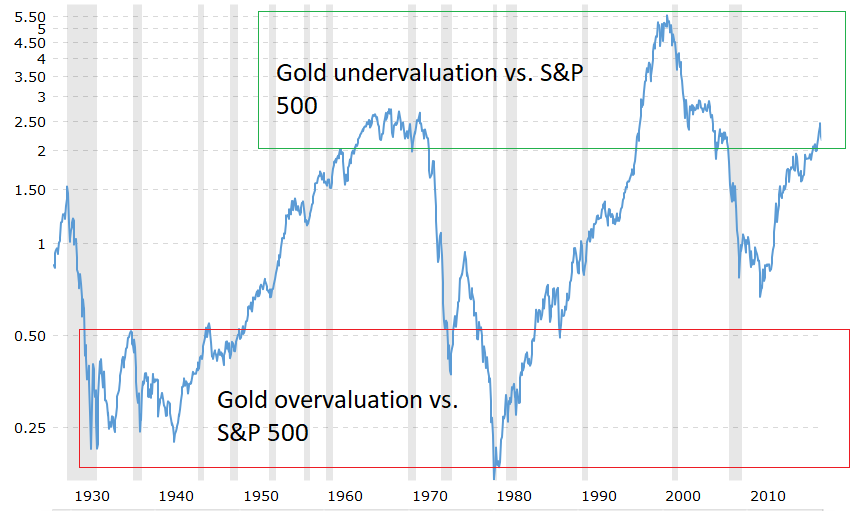

Here is the most obvious ratio. A comparison of gold to the S&P 500:

The value in gold at present market prices relative to the S&P 500 has only been matched in two decades prior: The 1960s and 1990s. Further, we have not seen relative overvaluation of gold in 40 years. The last period between overvaluation gaps in gold was 1940 – 1980, exactly 40 years. Needless to say, the gap is due to close, most likely through exponentially higher gold prices rather than a meltdown in the S&P 500.

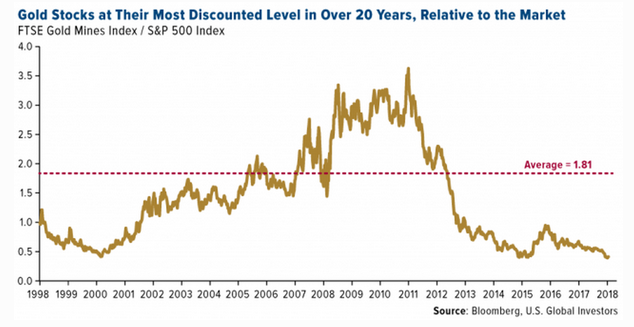

The next chart is an important one in terms of asset allocation within the gold sector. It measures the ratio between gold and the individual components that make up one of the more popular gold indices (HUI). Gold stocks have been completely abandoned by investors, while gold has remained at a relatively elevated price. This equates to the opportunity for gold investors being in individual gold miners as opposed to the physical metal itself. Gold stocks have rarely been cheaper from a historical perspective.

For further evidence of the despondency that currently exists among investors in the gold space, here is a comparison between the gold miners and S&P 500. Another multi-decade low in sentiment towards individual mining names.

Apart from an abundance of data showing that both gold and even more so, gold miners, are absurdly cheap. There is anecdotal data such as the fact that Vanguard recently changed their metals and mining fund name to the “Global Capital Cycles Funds,” taking down exposure to miners to just 25% of the fund from 80%. This leaves Vanguard investors, which, by the way is the largest mutual fund company in the world, with no way to participate in the advance of gold or gold miners. As an aside, the last time Vanguard made a similar move was in 2001, before the secular bull trend in gold started from $300. Needless to say, Vanguard follows demand by its investors. Investors have abandoned the sector, creating a highly asymmetric opportunity.

As is usually the case, investors tend to follow each other blindly over the proverbial cliff, without doing much in the way of thinking about liquidating asset classes that are either overwhelmingly in favor or taking positions in sectors that are overwhelmingly out of favor. This leads to vast discrepancies between price and actual value during periods of exuberant enthusiasm and despondent pessimism. The job of the investor is to capitalize on these discrepancies, which is often times an exercise in absolute isolation.

The act of buying into despondent pessimism is extremely difficult because you are effectively alone in your opinion, without evidence, other than your own, to substantiate a thesis. For a majority of investors, this is an extremely uncomfortable place. Others tend to thrive, seeking only situations where few other investors are present. T11's strategy dwells heavily in the latter discipline. Gold falls right into the classification of an extremely uncomfortable place where few other investors are present.

It doesn't simply stop at gold being a sentiment and value driven play. There are events unfolding in the geopolitical and macroeconomic landscape that leave very few scenarios where gold doesn't appreciate in value:

1. The Fed stops raising rates = dollar bearish/inflationary ramifications/bullish for gold

2. The Fed continues raising rates = substantially bearish for equities/inviting showdown with White House creating political instability/gold becomes an alternative asset class for investors seeking to hedge the instability

3. Quantitative tightening has just started to accelerate in Q4 2018, with the ECB joining the party with an accelerated QT in 2019 = compressed liquidity for global markets creating instability in global equities in developed markets/emerging market bullish/dollar bearish/gold bullish as it tends to rally in emerging market led economic advances

4. Any number of geopolitical scenarios involving Russia, China, the Middle East = gold will be seen as a safe haven asset

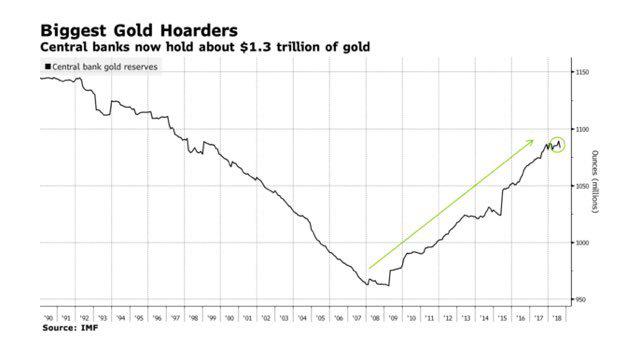

Perhaps the most interesting aspect of the current gold economy is the fact that global central banks, led by China and Russia, are hoarding gold for the first time in multiple decades. Ever since the financial crisis, global central banks have been steadily accumulating gold.

Most recently, the central bank of Hungary increased their gold holdings 10 fold to the highest level in 30 years. Poland made a similar move in recent months boosting central bank gold reserves to multi-decade highs. Obviously, central banks of Hungary and Poland play an insignificant role in the global central banking community. However, the general theme occurring here globally shouldn't be ignored.

Accompanying Hungary's first purchase of gold since the 80s was a press release from the central bank. Here is an excerpt:

Gold is not only for extreme market environments, structural changes in the international financial system, and deeper geopolitical crises. Gold also has a confidence-building effect in normal times, that is, gold can play a role in stabilizing and defending.

Gold is still considered to be one of the world's safest assets, whose characteristics can be attributed to gold's unique properties such as finite supply of physical gold, and lack of credit and counterparty risk given that gold is not a claim against a specific partner or country.

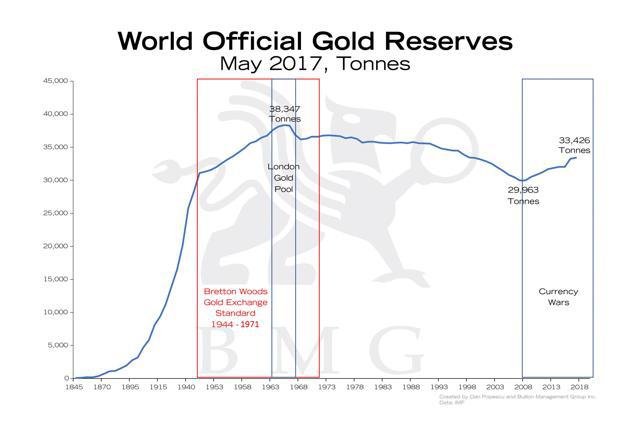

For greater context, below is a long-term look at world official gold reserves. The turn that took place in 2008 is the first time central banks have been accumulating gold since Nixon ended Bretton Woods, canceling direct international convertibility of the US Dollar into gold, effectively allowing the US to become the first country in history to be able to print an unlimited amount of currency to purchase goods.

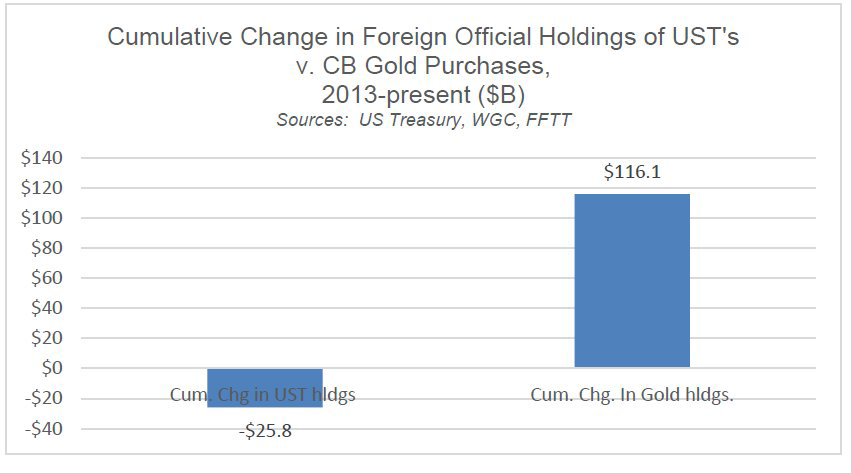

In recent years, the accumulation of gold has been accompanied by the liquidation of US Treasury securities.

This effectively amounts to global central banks, led by China and Russia, waging a financial war against the U.S. Dollar by pressuring the dollars reserve status through the simultaneous selling of US debt while steadily depleting physical gold reserves from the US and European pools.

This from a 2017 interview with macro analyst Luke Groman:

Timing any move in a macro asset class is an extremely difficult task. I want to be clear that this isn't a timing call, but rather a risk/reward call on gold as both an investable, uncorrelated asset and as a portfolio protection mechanism. It is akin to buying puts on the popular indices when the volatility index is in the single digits. Your cost to gain protection are extraordinarily attractive. This is currently the case with gold without the worry of time decay, with an optionality component attached in terms of upside

***

During November, I allocated 30% of the portfolios between two gold related names: 20% in SA (Seabridge Gold), 10% in GDX (Gold Miners ETF). I rarely will allocate into ETFs, however, gold miners are a can of worms, generally speaking, to research on an individual basis. The individual names are largely driven by the price of gold and different names possess substantial jurisdictional risk as many names have mines in Russia, Africa and Central/South America. The GDX etf is a means of allocating to the leading names in the mining sector.

SA is a junior gold miner, meaning that is basically a small-cap name within the space. Management at SA has been responsible in preventing the dilution of their shareholder base by issuing an abundance of shares as gold soared. Dilution is a common practice among gold miners as they tend to leverage a higher gold price into a myriad of projects, including mergers and developing new mines.

One of the likely reasons for the lack of dilution is that SA is heavily insider owned, with insiders holding approximately 30% of the shares. The largest outside shareholder of the name is Albert Friedberg who is one of the largest commodity focused hedge fund managers in Canada. He has been involved with the company since its inception in 1999.

Additionally, SA is highly levered to the price of gold itself, as it has a majority of its gold in the actual ground, owning the largest undeveloped reserve of gold in the world (KSM project located in northwest British Columbia) based on mineral reserves. In fact, on an ounce of gold to shares outstanding ratio, SA investors own more gold per share than any other public mining company. The company also has a pristine balance sheet, with plenty of cash and no debt. When gold begins moving, their reserves will become a primary target for other miners and/or a higher price will compel other miners to partner with SA, creating a stream of revenue for SA with minimal capital expenditures. SA can effectively be thought of a call option on gold that never expires or deteriorates in value due to time passed.

SA has estimated that the cost of constructing and operating a mine at their KSM facility is approximately $6 billion. In 2016 they completed a seven year long process of getting all the proper permits in place for mining KSM. According to the CEO of the company, other large miners have been approaching SA offering to co-develop KSM, but SA has yet to receive the right offer.

There are only a handful of miners, such as Newmont and Barrick Gold, that can afford to put up the capital in order to construct such a large scale mining project. SA has already stated they do not have the financial capacity to build out the mine on their own. The spark that ignites interest in building out the mine on SA's terms will be a gold price that makes extracting gold from the site a virtual no-brainer. A price per ounce above $1,500 assuredly accelerates discussions with interested parties.

In the meantime, we have a responsible management team, invested alongside shareholders, who have demonstrated their ability to keep shareholders whole, minimizing dilution, while they wait for the gold they have in the ground to appreciate in value to the point they can begin extracting it. The upside in this case is substantial, as there are more than a few asymmetric factors at work, with the expectation that physical gold has found its base.

_______________________________________________________________________________

From time to time, I email individual company research, commentary and excerpts from my monthly investor letter to those who are interested. If you would like to receive future emails, please write me at mail@T11Capital.com

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.