In order to understand the current market framework, an investor must disavow a handful of consensus opinions that are being regarded as fact:

1. This is not a bear market

2. Poor economic performance over the next few months doesn't necessarily equate to poor stock market performance

3. Far from being irrelevant and out of ammunition, the Fed is more relevant than ever

4. There is no historical reference to this market. It is completely unique and unprecedented in scope. Future results will reflect this fact.

As dynamic as the markets are, Wall Street remains stale in more ways than one. Given recent events, the most obvious example is the rigid definition of a bear market, claiming that a fixed percentage decline constitutes a bear market irrespective of the pace of that decline or the environment in which the decline occurred.

While labels may not matter in many situations, when a market is labeled a “bear market” then investors are prone to make historical references to prior real bear markets. When you compare a real secular bear market of prolonged length to what has a high probability of simply being a steep correction within a secular bull market, then your results will be flawed right from the onset.

Nearly every piece of analysis that is emerging from Wall Street currently assumes that this is the beginning of a prolonged bear market, waving goodbye to the days of prosperity that are now far in the rear view mirror. From this foundation, accurate future results cannot be attained.

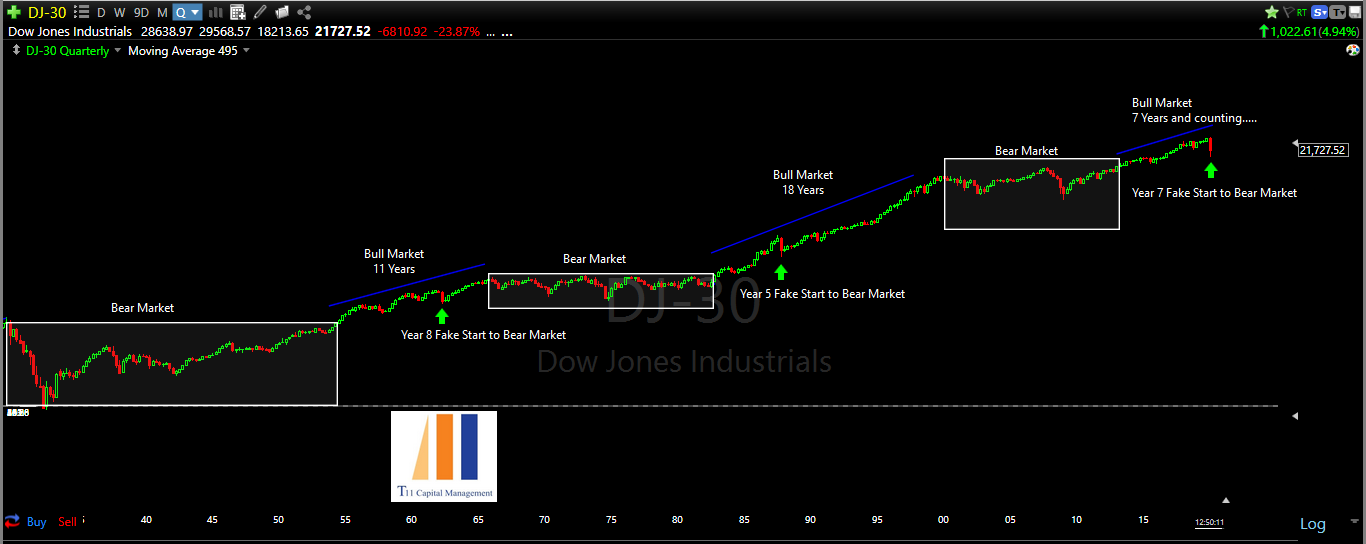

How do we know that this is not a bear market? Over the past nearly 100 years, there have three secular bull markets. We are currently in the third secular bull market of the post-Great Depression era. Within these secular bull markets, each and every one has had one or more false bear market signals that caused investors to regrettably give up on the secular bull market prematurely. In the prior two secular bull markets, year 8 and year 5 of the secular bull saw dramatic declines.

In the first secular bull market of the post-Great Depression era in 1962, the Dow declined 30% over a six month period, before continuing its rise, with a gain of 100% over the next three years. The 30% decline occurred in year 8 of the secular bull market.

In the second secular bull market, beginning in 1982, in the 5th year, we had the 1987 crash, with a 41% decline from peak to trough. In three years time, the market was again 100% higher.

We are presently in the 7th year of this secular bull market, having experienced a 38% decline from peak to trough in the Dow over the past two months. This fits right in with prior mid-cycle declines. The chart below provides an exact roadmap of where we are within this secular bull market. Keep in mind that secular bull market cycles are expansionary in nature, meaning that this secular bull market should be greater in length that the prior two, especially given the monetary and fiscal intervention. In other words, this current bull market should last well past 2030.

The greatest legacy of the virus we are all currently dealing with will not be perpetual elbow bumps or hand sanitizer dispensers strapped around each of our necks. Rather, the greatest legacy will be that the virus greatly accelerated the creation of inflation within the economic system via persistent monetary tinkering and the creation of an ever present social safety net guaranteeing American's income.

With QE beginning during the financial crisis in 2008, the Fed has come to the correct conclusion that they can inflate asset prices in order to create economic prosperity. However, in recent years a very big problem has arisen in the form of economic inequality suffered by those who are not in possession of inflating assets, while having their wages stagnate.

The virus has allowed the cover of a health crisis that has morphed into an economic crisis to begin the rollout of what will likely be an ever-present fiscal stimulus package, providing a reasonable amount of income for individuals and families, striking the perfect balance between maintaining social order and allowing for greater economic prosperity.

Once a government learns how to inflate assets at will, then the only impediment towards achieving near perpetual prosperity is greater economic disparity. At the same time, it seems that the Fed and Treasury have correctly come to the conclusion that the same mechanism used to inflate asset prices can be used to inflate individual checking accounts, allowing consumers to pay for basic expenses while producing very little or in most cases, absolutely nothing.

This new dynamic, ushered in very quickly by the virus, creates an entirely new economy than anything we have been used to in the past, the most obvious ramification of which will be inflationary in nature. When newly printed cash is put in the checking accounts of individuals who are not pulling their weight in the economy by producing anything, then the output of goods falls while everyone has cash in their checking accounts to purchase more goods. The natural effect of this will be that prices for everything will rise.

When cash is produced in this nature to inflate everything from assets to the price of consumer goods via direct deposits to individual checking accounts, cash becomes worth less and less over time. The accelerating nature of this dive towards worthlessness will be the biggest economic consequence and theme of the next decade.

In the near term, we have the prospect of increasingly bleak economic reports over the next few months, which the market has gone to great lengths to discount, being all but factored in at this point.

In the weeks and months ahead, the markets will be factoring in the following sets of data:

1. Pent up demand leading to a near euphoric spending blitz as consumers are let out of their cages with fresh cash to spend.

2. An entirely new set of job opportunities that will be created as a result of consumer habits that have been altered due to the virus.

3. Increasing earnings in technology related issues as businesses increase efficiencies as a result of lessons learned during the virus crisis.

All of this is coming against a backdrop of a Federal Reserve guaranteed economic backstop. A majority if not all of the bearish arguments pertaining to what will cause the next great long-term bear market have been dealt with by a Fed backstop.

The rolling over of massive amounts of corporate debt with no demand? The Fed's got it.

Liquidity to provide businesses? The Fed's got it.

Mortgage market freezing up? The Fed's got it.

Consumers not having money for basic expenses? The Fed's got it.

Deflationary forces rampaging through the economy? The Fed took out their inflation bazooka.

Municipal and State financial troubles? The Fed's got it.

Everything is backstopped. It is infinite in nature. The grand QE experiment is entering its next phase.

What's perhaps most perplexing in the face of all of these facts is the insistence of a vast majority of analysts and investors to attempt a comparison of this market to any other in history. The number of references to past corrections and bear markets, be it 1929, 1987 or even 2018 are so far off base that they should be disregarded completely.

The very unique nature of this market was revealed by the historic speed with which this correction took place. The fastest decline from an all-time high ever. Yet the natural impulse of investors is to take that information and attempt to compare this market with markets of the past. It's like Ferrari rolling out a new car that just did 0-60 in 2 seconds and prospective buyers deciding to take out an old of issue of Car and Driver to compare the car to a 1986 Camaro.

To be clear, there is no comparison to the current market. Every historical comparison will mislead investors into what will likely be an erroneous conclusion. The market velocity on the upside will continue to accelerate, as there are an entirely new set of dynamics at work in the form of global central bank intervention in the markets that will continue to make markets behave in an unprecedented manner.

The action for investors here is abundantly clear. Equities are currently sitting at a 30% discount from their all-time highs a little over a month ago, with an economy that is backstopped by an infinite Fed balance sheet while at the same fiscal stimulus measures are to be rolled out in stages throughout the year. Cash will be worthless in such a scenario other than provide the illusion of safety. More than anything, investors should be as aggressive as possible in allocating to U.S. equities at this point in time.

Zenolytics now offers Turning Points and ETF Pro premium service Click here for details.

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.