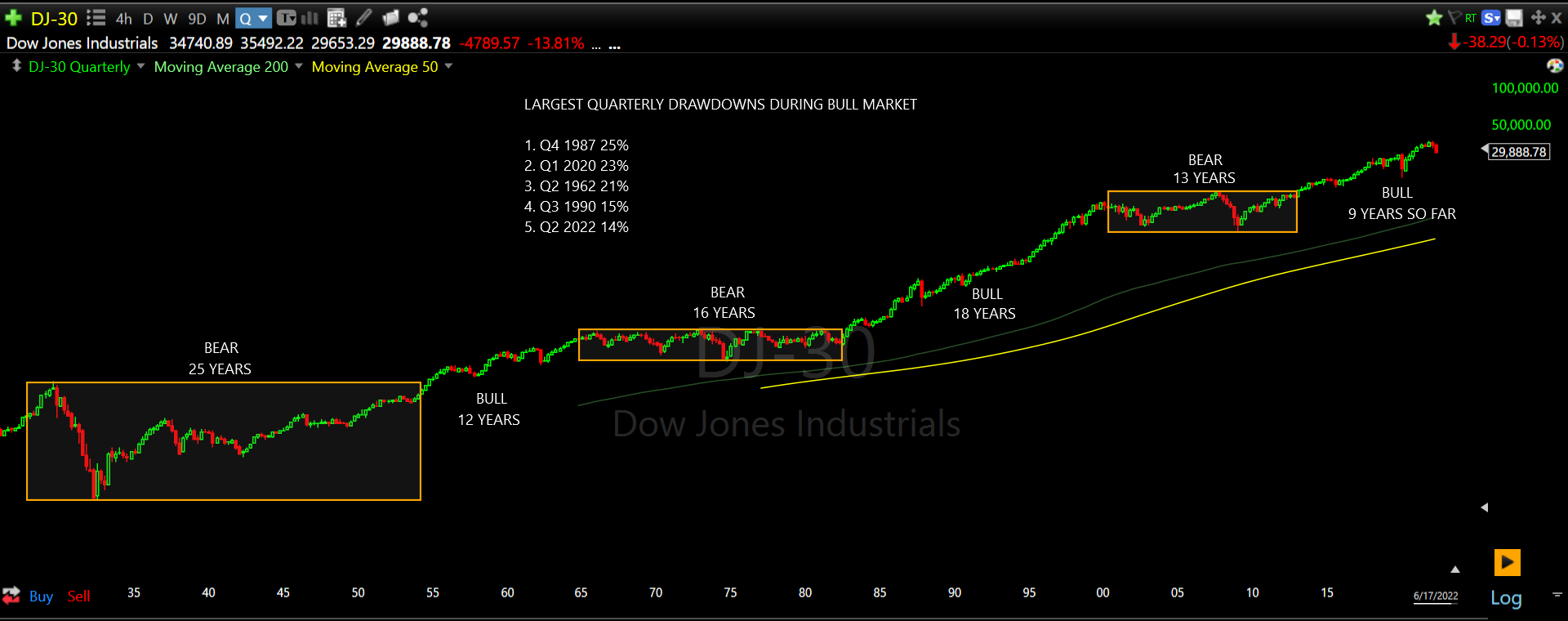

Those of you who have been familiar with my work over the years will recognize the following chart. I post it from time to time when emotions, psychological handicaps and all around pandemonium breaking loose becomes the theme of the day, week, month or quarter.

This is a 100 year chart of the Dow showing bull and bear markets of the past and present, revealing some valuable data applying to the current situation we find ourselves in:

We are presently 9 years into this bull market, making it a relatively young bull market compared to those of the past. The threat of this being some type of diabolical generational top, with the Dow crashing to 5000 in the years ahead is slim to none, with a strong tilt towards none.

What is more interesting, however, is when you consider the fact that we have been unlucky enough over the past couple of years to experience two of the most vicious quarterly declines of a bull market over the past 100 years.

I am, of course, referring to the 2020 pandemic decline of 23% and the current 2022 inflationary/fear of recession decline of 14%. Ranked 2nd and 5th respectively over the past century.

What is interesting is that we have a corollary to this period from 1987 to 1990.

In 1987, the infamous Dow crash took place, making it the worst bull market quarter in history with a decline of 25%.

Just a few years later, similar volatility struck in 1990 with recessionary fears driving the Dow down by 15%.

Judging from history, it's rare during a bull market to see such compacted volatility events.

Here is what the Dow looked like from the 25% 1987 crash to the 15% 1990 mini crash:

Here is what the current market looks like from the Q1 2020 crash to the current Q2 2022 mini crash:

What is interesting to note is that following the Q3 1990 mini crash, the Dow reached a brand new all-time high just six months later, emphasizing the point that market cycles matter much more than you, I or anyone else thinks.

Oh but the Fed wasn't tightening back then and inflation wasn't out of control, you say?

Sure, it was a different situation entirely, but the situation then was arguably much worse, with a banking crisis via the savings & loan crisis resulting in the collapse of hundreds of banks, further resulting in the insolvency of the Federal Savings and Loan Insurance Corporation. Followed by a recession that lasted from 1990-1991.

Despite all of this upheaval, the markets managed to forge ahead to new highs, despite getting knocked down in what was one of the worst quarters in bull market history as the market naturally reacted to the highly negative news flow.

This makes the current situation, with the S&P at 3674 as binary as it gets.

You have two options as a matter of belief moving forward and only two:

- You believe this has been the shortest secular bull market in history, with the market making a multi-year high early this year, only to suffer further for years on end as we move into a prolonged bear market.

- You believe that this is a 1990 type of scenario, where back to back volatility crashes during a two year window taking place within a secular bull market have created what is the best buying opportunity since March 2020. A buying opportunity that I highlighted, by the way, in a note on March 29th, 2020 titled "It's Time For Investors To Go All In On Equities."

This is no different than March 29th, 2020 or October of 1990. Investors are drinking the bearish juice. They cannot see the forest for the trees. They have forgotten that market cycles matter much more than any pseudo-understanding you may think you have of Fed policy, economic cycles, geopolitics or earnings forecasts moving forward.

Investing all comes down to a few moments, this is one of them.

Unabashedly, blatantly bullish at S&P 3674, with new highs coming much faster than anyone can imagine.

Disclaimer

This website is for informational purposes only and does not constitute a complete description of our investment advisory services. No information contained on this website constitutes investment advice.

This website should not be considered a solicitation, offer or recommendation for the purchase or sale of any securities or other financial products and services discussed herein. Viewers of this website will not be considered clients of T11 Capital Management LLC just by virtue of access to this website.

T11 Capital Management LLC only conducts business in jurisdictions where licensed, registered, or where an applicable registration exemption or exclusion exists. Information contained herein is not intended for persons in any jurisdiction where such distribution or use would be contrary to the laws or regulations of that jurisdiction, or which would subject T11 Capital Management LLC to any unintended registration requirements. Visitors to this site should not construe any discussion or information contained herein as personalized advice from T11 Capital Management LLC. Visitors should discuss the personal applicability of the specific products, services, strategies, or issues posted herein with a professional advisor of his or her choosing.

Information throughout this site, whether stock quotes, charts, articles, or any other statement or statements regarding capital markets or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in, the transmission thereof to the user. With respect to information regarding financial performance, nothing on this website should be interpreted as a statement or implication that past results are an indication of future performance.